Keep in Touch – Client March 2024

March 10, 2024Keep in Touch – Client October 2024

October 30, 2024Welcome back to our loyal clients and welcome to our new clients. Thank you for choosing Jones Insurance.

So I promised in our last newsletter that I would get back from my insurance meeting in Vancouver with some great one liners… here you go, my favourites first…

- Every heartbeat counts, so don’t waste them.

- Your life is like an egg, great things begin on the inside.

- We are more alike than we are different, perspective matters, live life well.

- Say no to something in the next 7 days, Build a “no muscle.”

- Preparation makes you great – Over prepare!

Hopefully one or two of these resonates with you.

Now to insurance ..

Have you booked an insurance review with us in the last 2 years? If not I’m sure something has probably changed in your life that will affect your financial plans and your insurance needs. Has your income changed? Do you remember the benefits that your current insurance policy offers?

Is it time to look at income protection or better cancer cover?

If you would like to book an insurance review, please email Jayne at info@jonesinsurance.co.nz to set up a time that suits you to chat with me. We will lock it in.

Thank you so much for trusting me and Jones Insurance to continue looking after your personal insurance plan – please do keep in touch.

In this issue we’ll be looking at:

- How Premiums are Calculated

- Income Protection Cover

- Managing claims and policy alterations with NIB

- Recipe of the Month: Avocado Pasta

Enjoy your day,

Paula Jones

FSP82763

What is Income Protection?

Income Protection protects your most valuable asset – your future income.

It provides a financial safety net should you be disabled as a result of sickness or injury and unable to earn your regular income. The monthly benefit helps replace a significant portion of the lost income to help maintain your usual lifestyle during treatment and recover.

How long will you income continue if you are ill or unable to work?

Managing claims and policy alterations with NIB

NIB re-launched the member portal and the mynib app a few months ago and its functionality is second to none. Members can submit a claim, submit a pre-approval, update their personal details, make changes to their cover (including excesses) and change payment details. They can also complete a personalised health check and find a health provider.

It’s really easy to navigate and find your way around. Below are some screen shots from the mynib app:

The best thing about it is the engine that runs this functionality can make decisions and take actions to process the claim/query efficiently and quickly. If it can’t take the necessary action it will send the query to the relevant team for them to process.

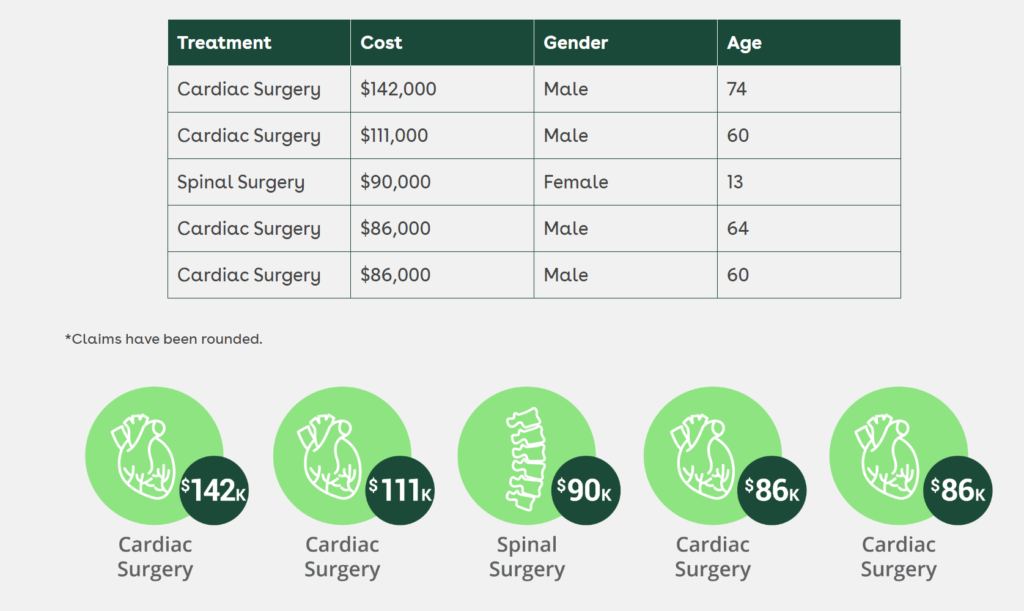

NIB’s Top 5 Claims – June 2024: